What is a Testamentary Trust?

What is a Testamentary Trust?

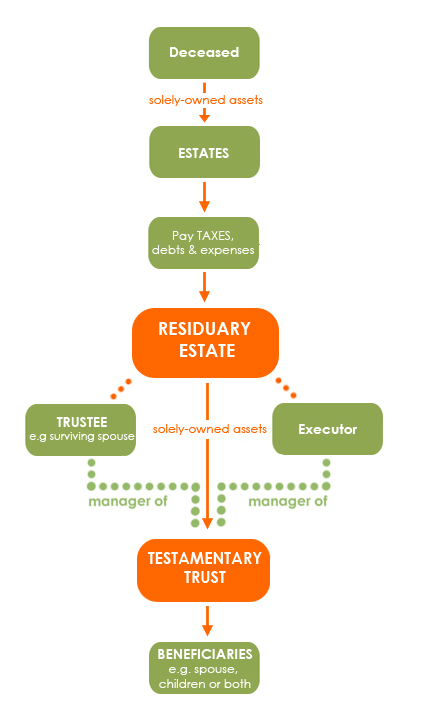

A Testamentary Trust is a Trust created under a Last Will and Testament – hence the name Testamentary. It only comes into effect upon the death of the Willmaker. The assets that are personally owned by the Willmaker will pass into the Trust.

Executors of the Will often become the Trustees of the Testamentary Trust. However, if you have children or other beneficiaries who are adults, you can appoint them to be the Trustee of their own Trust.

Testamentary Trusts can take many forms, but the most popular is the fully discretionary Testamentary Trust. The main benefits of a discretionary Testamentary Trust are tax savings and improved asset protection.

Tax Savings

Testamentary Trusts are useful to minimise income tax liabilities payable by your beneficiaries in the years after your death.

Testamentary Trusts allow income from the inheritance to be split among beneficiaries across many financial years. Generally, if your beneficiary has one or more child or grandchild under the age of 18, and/or a spouse who does not work full time, this will translate into significant tax savings.

A significant benefit is that minor beneficiaries of a Testamentary Trust are treated as adults for tax purposes. This means that they can receive, on current tax rates, up to $18,200 per year tax free. This is a special exception to the normal tax rules.

The Capital Gains Tax rules generally apply in the same way to Testamentary Trusts as they do to individuals. That is, a Testamentary Trust is entitled to “rollover relief” upon the transfer of assets from a deceased Estate, and to a 50% Capital Gains Tax discount upon the subsequent sale or disposal of those assets.

Improved Asset Protection

Discretionary Testamentary Trusts (which leave it up to the Trustee to decide who is to receive payments of income and capital and in what proportions) can provide greater asset protection in the event of a marriage breakdown or bankruptcy of a beneficiary.

The spouse of a beneficiary can be excluded from receiving any capital or income from the Trust in the event of a later separation. This will significantly improve the beneficiary’s chances of retaining his or her inheritance in the event of a divorce.

Beneficiaries who operate their own businesses will also benefit from improved risk protection if their inheritance is received within a Testamentary Trust.

Testamentary Trusts can continue for many years and be passed “down the blood line” to your direct descendants, meaning that your assets remain in the family from generation to generation. An inheritance held within a Testamentary Trust will be considered by the Family Court as a financial resource.

Katrina Jacobs Estate Law can discuss with you whether a Testamentary Trust should be put in place in your particular circumstances and in light of your estate planning needs.